What Mid-Year Market Volatility Means for Your Portfolio

As we reach the midpoint of the year, many investors find themselves checking their portfolios more frequently than usual. Headlines about inflation, interest rates, geopolitical conflicts, government policy, and corporate earnings can create an unsettling environment where daily market swings seem larger than life. It’s natural to wonder whether it’s time to make changes or simply wait for the uncertainty to pass.

While market volatility can be uncomfortable, it is also one of the most normal—and expected—parts of investing. History has consistently shown that periods of uncertainty are temporary, while disciplined investing has remained one of the most reliable paths to long-term wealth creation.

Understanding what volatility means, how to respond thoughtfully, and why maintaining a long-term perspective matter can help investors avoid costly emotional decisions and remain focused on their financial goals.

Volatility Is a Normal Part of Investing

Market volatility refers to the degree to which investment prices fluctuate over time. Some years experience relatively calm markets, while others include significant swings both upward and downward.

Although sudden declines often dominate financial news coverage, they are far from unusual. In fact, the stock market experiences corrections and pullbacks on a regular basis.

Historically:

- Market declines of 5% occur frequently during most years.

- Historically, the stock market experiences regular pullbacks. For example, according to data from Capital Group analyzing the S&P 500 Index from 1952 through 2025, market corrections of 10% or more occurred approximately once every two years on average.

- While bear markets (declines of 20% or more) are a challenging part of investing, historical data from Hartford Funds shows that every S&P 500 bear market from 1928 through 2025 was eventually followed by a recovery.

Note: Past performance does not guarantee future results.

These fluctuations are simply the price investors pay for pursuing higher long-term returns. Markets constantly adjust to new information including economic data, corporate earnings, interest-rate expectations, political developments, technological innovation, and investor sentiment.

While short-term movements often feel dramatic, they rarely alter the long-term trajectory of well-diversified portfolios.

Why Volatility Feels So Uncomfortable

Behavioral finance teaches us that investors experience the pain of losses much more intensely than the satisfaction of equivalent gains. A portfolio decline of 10% often creates significantly more emotional discomfort than a subsequent 10% gain creates happiness.

This phenomenon can lead investors to make emotionally driven decisions such as:

- Selling after markets have already fallen

- Moving entirely into cash

- Waiting for “certainty” before reinvesting

- Chasing investments that recently outperformed

- Constantly changing long-term investment strategies

Unfortunately, these reactions often lock in temporary losses and cause investors to miss the strongest periods of recovery.

Markets frequently rebound before economic headlines improve. By the time investors feel comfortable returning to the market, much of the recovery has already occurred.

Emotional Reactions vs. Rational Responses

Periods of volatility often separate emotional investing from disciplined investing.

An emotional reaction typically focuses on today’s headlines and immediate uncertainty. Investors may believe that “this time is different” and attempt to avoid additional losses by selling investments.

A rational response begins by asking different questions:

- Have my long-term financial goals changed?

- Has my investment time horizon changed?

- Has my tolerance for risk permanently changed?

- Has the underlying investment thesis changed?

If the answer to these questions is “no,” then temporary market declines generally do not require major portfolio changes.

Instead, volatility often presents an opportunity to review financial goals, evaluate portfolio allocations, and ensure investments remain aligned with an investor’s long-term plan.

Successful investing is often less about predicting markets and more about maintaining discipline when uncertainty is highest.

Diversification Remains One of Your Best Defenses

One of the most effective ways to manage market volatility is through diversification.

Diversification means spreading investments across different asset classes, industries, sectors, company sizes, and geographic regions rather than relying on a single investment or market segment.

A diversified portfolio may include:

- U.S. large-cap stocks

- Mid-cap and small-cap stocks

- International developed markets

- Emerging markets

- Investment-grade bonds

- Short-term fixed income

- Real estate investments

- Cash reserves for short-term needs

Because different investments respond differently to changing economic conditions, diversification can help reduce the impact of any one area experiencing significant losses.

While diversification cannot eliminate risk or prevent market declines, it has historically reduced portfolio volatility while maintaining long-term growth potential.

The Value of Rebalancing

Market volatility also creates opportunities to rebalance portfolios.

Over time, market movements naturally shift portfolio allocations. For example, after a strong stock market rally, equities may represent a larger percentage of a portfolio than originally intended. Conversely, after a market decline, stocks may represent a smaller allocation.

Rebalancing involves periodically returning investments to their target allocation.

This disciplined process encourages investors to:

- Sell portions of investments that have appreciated significantly.

- Purchase investments that have temporarily declined.

- Maintain the intended level of portfolio risk.

Rather than attempting to predict market direction, rebalancing follows the simple discipline of buying relatively low and trimming positions that have become relatively expensive.

Over many market cycles, this process has helped investors maintain appropriate risk levels while removing emotion from investment decisions.

Staying Invested Matters

Perhaps the greatest danger during volatile markets is missing the recovery.

Some of the market’s strongest days historically occur immediately after periods of steep declines. Investors who move to cash often miss these rebounds because they wait for confirmation that conditions have improved.

Market timing can be costly. For example, according to the J.P. Morgan Asset Management 2026 Guide to the Markets, an investor who missed just the 10 best-performing days in the S&P 500 Index over the 20-year period from January 1, 2006, through December 31, 2025, would have seen their overall annualized return reduced by more than half, assuming fully reinvested dividends. Remaining invested allows portfolios to participate in both recoveries and long-term market growth.

Time in the market has historically proven far more valuable than attempting to perfectly time market entry and exit.

History Provides Valuable Perspective

Although every market downturn feels unique, history provides reassuring perspective.

The Dot-Com Crash (2000–2002)

Following years of rapid technology stock appreciation, markets declined sharply when the technology bubble burst. Many investors questioned whether technology companies would ever recover.

While numerous speculative companies disappeared, diversified investors who remained invested eventually benefited from one of the strongest multi-year bull markets in history.

The Global Financial Crisis (2008–2009)

The financial crisis brought widespread fear, collapsing housing prices, banking failures, and severe economic recession.

The S&P 500 declined by more than 50% from its peak before beginning a powerful recovery in March 2009.

Investors who maintained diversified portfolios and continued investing throughout the downturn ultimately experienced significant gains during the following decade as markets reached repeated record highs.

The COVID-19 Market Decline (2020)

The onset of the COVID-19 pandemic produced one of the fastest bear markets in modern history. Global markets fell sharply amid widespread uncertainty and economic shutdowns.

Yet the recovery was equally remarkable. Major stock indexes regained their losses within months, and many reached new all-time highs sooner than many experts expected.

Few investors could have accurately predicted either the speed of the decline or the pace of the recovery.

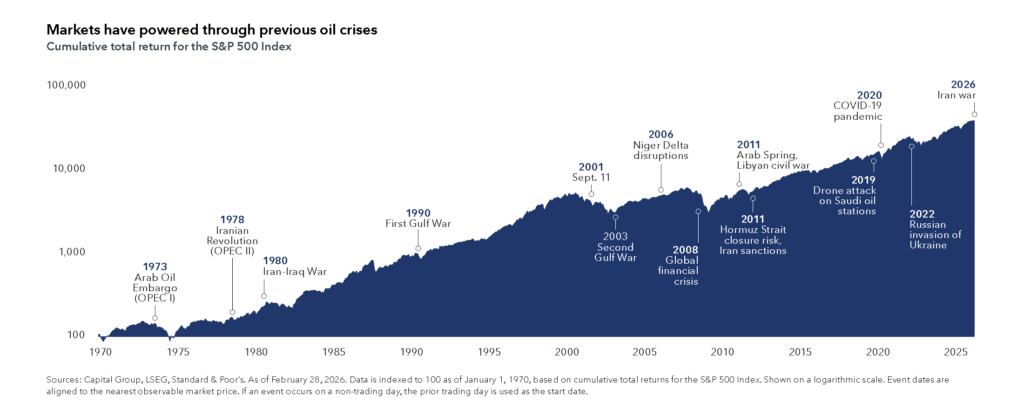

Geopolitical Shocks and Energy Crises

Sudden international conflicts and resulting energy price spikes have historically triggered localized market anxiety and fears of economic slowdown. From the Arab Oil Embargo in 1973 and the Iranian Revolution in 1978 to the more recent conflicts in 2026, disruptions to the global energy supply have regularly caused short-term volatility.

While these periods of escalating energy costs often create near-term uncertainty for businesses and consumers, historical data demonstrates that markets have consistently powered through oil-related crises. Investors who avoided reactive decision-making and maintained their long-term allocations typically saw equity markets absorb the shocks and continue their upward trajectory over time.

The lesson remains clear: markets have consistently demonstrated resilience despite wars, recessions, inflation, financial crises, pandemics, and political uncertainty.

Focus on What You Can Control

While investors cannot control market performance, they can control many of the factors that contribute to long-term success.

These include:

- Maintaining an appropriate asset allocation.

- Keeping investment costs low.

- Diversifying broadly.

- Rebalancing periodically.

- Continuing regular contributions.

- Minimizing taxes where appropriate.

- Avoiding emotional investment decisions.

- Reviewing financial goals annually.

These decisions often have a greater impact on long-term investment outcomes than attempting to predict short-term market movements.

Looking Beyond Today’s Headlines

Market volatility is never enjoyable, but it is an unavoidable part of successful long-term investing. Every period of uncertainty eventually becomes another chapter in market history, while disciplined investors who stay focused on their goals are often rewarded over time.

Rather than viewing volatility as something to fear, investors can view it as a reminder that markets are dynamic, expectations constantly evolve, and patience remains one of the most valuable investment assets.

As we move through the remainder of the year, remember that successful investing isn’t about avoiding every downturn—it’s about having a thoughtful plan, remaining disciplined during periods of uncertainty, and allowing time and compounding to work in your favor.

While no one can predict exactly what the coming months will bring, history offers a consistent message: markets have recovered from every major downturn, and long-term investors who remain diversified, rebalance thoughtfully, and stay invested have generally been well positioned to participate in those recoveries.

Insight Wealth Strategies, LLC is a Registered Investment Adviser. Advisory services are only offered to clients or prospective clients where Insight Wealth Strategies, LLC and its representatives are properly licensed or exempt from licensure. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. No advice may be rendered by Insight Wealth Strategies, LLC unless a client service agreement is in place.

Insight Wealth Strategies, LLC (IWS) and its affiliates do not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Reviewed by,

Andre Paiva, CRPC®

Lead AdvisorAndre joined Insight Wealth Strategies in 2018 and works as a Lead Advisor on our Advisory team creating financial plans and implementing investment management strategies for our clients. His primary area of expertise lies in retirement planning with a focus on developing retirement income strategies, corporate benefit analysis and stock option planning. He holds a Bachelor’s degree in Business Management from University of Phoenix.

Related Blogs

Executive Work Life Balance Strategies for Long-Term Success

Stay informed with our latest insights on

wealth management for pre-retirees.

Subscription Form

Ready to plan your retirement transition?

The decisions you make in the next few years will determine your retirement lifestyle. Let’s create a plan that gives you confidence in your financial future.