Segment Rate Newsletter

Segment Rate Update –

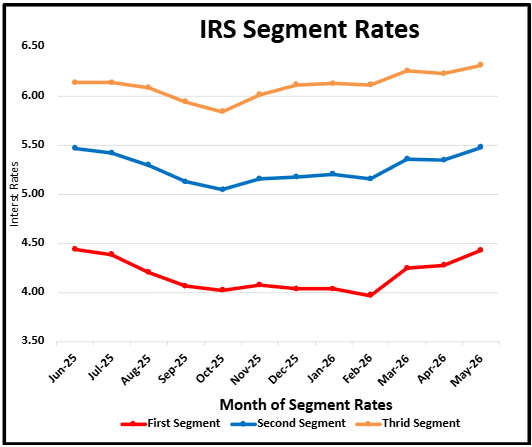

May 2026 Numbers

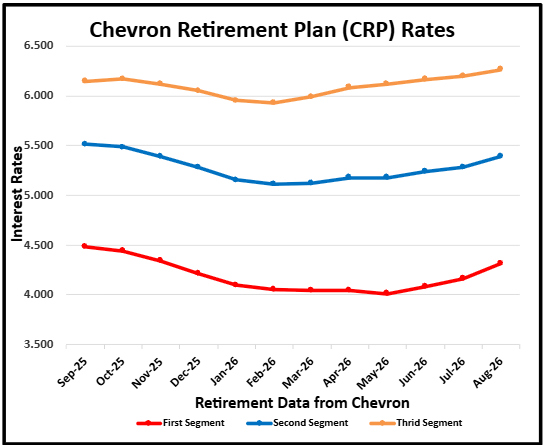

The following table demonstrates the hypothetical* impact of recent IRS segment rate updates on the lump sum value for a 65-year-old Chevron employee with an estimated single-life annuity payment of $7,500/month:

If a Chevron employee is deciding between a July 2026 or August 2026 benefit commencement date, based solely on the CRP lump sum value, July would be the more favorable option. In this hypothetical scenario, the approximate decrease in CRP value for an August retirement would be about -0.92%.

While your CRP Lump Sum or pension is influenced by more than just interest rates, reviewing recent rate trends can help you understand potential impacts and make a more informed retirement date decision. Keep in mind that interest rates have an inverse relationship with lump sum pension values—when interest rates increase, lump sum values decrease.

| August 2026 | Change From Previous Month | July 2026 | Change From Previous Month | June 2026 |

|---|---|---|---|---|

| $1,036,538.35 | -$9,558.62/-0.92% | $1,046,096.96 | -$4,442.03 / -0.42% | $1,050,538.99 |

*Due to the individualized nature of CRP lump sum calculations, you would need to run the estimator to determine the actual impact on your specific value.

Note: Guidance for Standard Deduction, Earned Income Credit, and potential refund changes can be found on the IRS website.

Watch Our Webinar!

Understanding Segment Rates: “Am I Working for Free?”

With interest rates on the rise, many Chevron employees are asking themselves, “Am I working for free?”

If retirement is on the horizon, choosing the right month to commence benefits can be more complex than it may seem.

We break down how segment rates work, how they impact your lump-sum payment, and why the timing of your retirement matters.

Our Chevron financial advisors have over 20 years of experience helping employees navigate retirement and maximize their benefits.

Segment Rate FAQs

A segment rate is an interest rate used by the IRS to determine the present value of future pension payments. These rates are divided into short-term, mid-term, and long-term segments, each applying to different time periods of expected payments.

A segmented pension refers to a pension plan that uses segment rates to calculate lump-sum distributions. The pension’s value is determined using different interest rates for different time periods, influencing how much a retiree receives in a lump-sum payout versus annuity payments.

The IRS determines minimum present value segment rates based on corporate bond yields. These rates are published monthly and help define the discount rates used to calculate pension liabilities and lump-sum payouts.

The IRS publishes segment rates on a monthly basis, typically around the middle of each month. These rates are released in IRS notices and are used to calculate pension funding obligations and lump-sum distributions.

Interest rates can be categorized into:

- Segment rates (used for pension calculations)

- Federal Reserve rates (impacting overall borrowing costs)

- Corporate bond rates (affecting investment returns)

- Fixed and variable rates (common in loans and mortgages)

Segment rates directly impact the lump-sum value of a pension. When rates increase, the present value of future pension payments decreases, leading to lower lump-sum payouts. Conversely, lower rates result in higher values.

Sign up below to have updated Segment Rates delivered directly to your inbox

Subscription Form

Ready to take control of your financial future?

The decisions you make in the next few years will determine your retirement lifestyle. Let’s create a plan that gives you confidence in your financial future.

IWS does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to this website or incorporated herein, and takes no responsibility therefor. All such information is provided solely for convenience purposes, and all users thereof should be guided accordingly.