Year-End Tax Planning: Top Strategies for 2025

Year-End Tax Planning: Top Strategies for 2025 As the year comes to a close, it’s

Year-End Tax Planning: Top Strategies for 2025 As the year comes to a close, it’s

Why it’s Hard to Stay Disciplined in Volatile Markets A long-term retirement investment strategy, resulting

Why Having an Investment Plan is Important What is Investment Planning? Investment planning is a

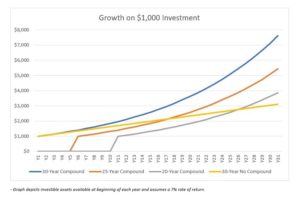

Utilizing the Power of Compound Interest For investors, there is unfortunately no magic wand or

Understanding the Required Minimum Distribution In an effort to encourage workers to save for retirement,

Understanding Stock Market Corrections: What Every Investor Should Know What is a Stock Market Correction?